Audio dialogue

🎧 Listen to the Audio Dialogue

This audio dialogue was generated with AI from this article and is provided for general information only — it is not financial advice, and availability, amounts, structures, and terms depend on each business’s circumstances and are subject to review and approval.

The software you used to log into is becoming software that runs itself. As the “agent economy” rewires how businesses operate — and levels the playing field for owners and advisors alike — the question shifts from which tools you buy to how you fund the edge they create.

In April 2026, Salesforce co-founder Parker Harris asked a question that should stop every operator in their tracks: “Why should you ever log into Salesforce again?” It wasn’t a provocation. It was a strategy. With Headless 360, Salesforce made every capability in its platform available as an API, an MCP tool, or a CLI command — so an AI agent can resolve a case, update a deal, or deploy a change without a human ever opening a browser. The interface, the thing we’ve equated with “software” for forty years, is dissolving.

This is the agent economy, and it is not a feature release. It’s a phase change in how work gets done — and, for the businesses living through it, a once-in-a-generation question about capital.

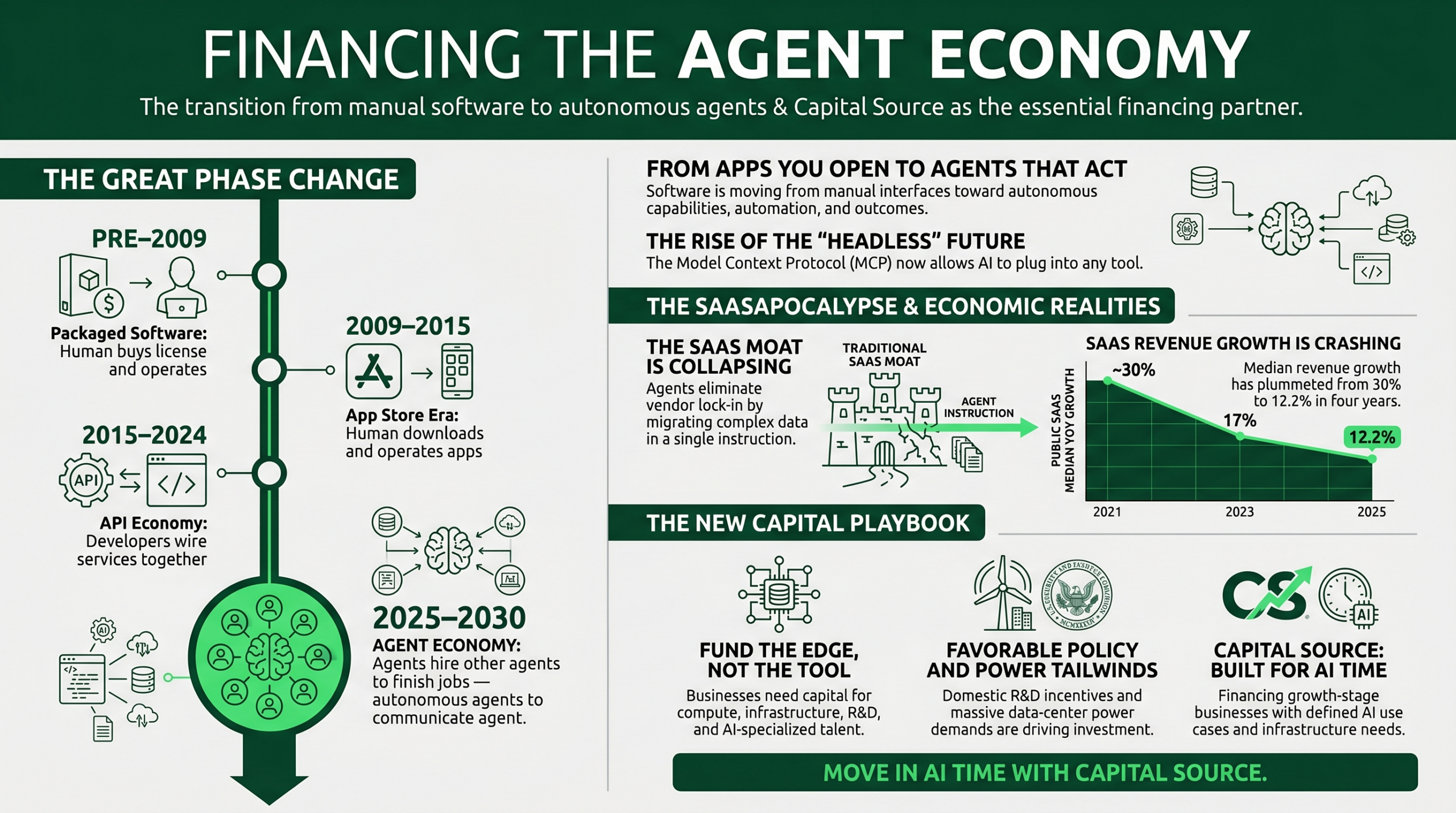

From apps you open to agents that act: four eras of software

To see where this goes, look at where it’s been.

The connective tissue making this possible is the Model Context Protocol (MCP) — an open standard introduced by Anthropic in late 2024 and often called “USB-C for AI.” Before USB-C, every device needed its own cable; MCP gives any AI model a single, standard way to plug into any tool or data source. Adoption was almost instant: OpenAI, Google, and Microsoft aligned on it within months, it now governs through the Linux Foundation, and by the end of 2025 it counted roughly 97 million monthly SDK downloads and more than 10,000 public servers. Salesforce’s Headless 360 — 60+ MCP tools and 30+ ready-made skills usable directly inside agents like Claude Code and Cursor — is simply the largest enterprise platform admitting the obvious: the future is headless.

The playing field just leveled

Here’s the part that matters for Main Street. The same frontier models powering enterprise agents — ChatGPT, Claude, Perplexity — sit in the pocket of every business owner, for the price of a phone bill. The capability gap that used to separate the well-resourced from everyone else has narrowed to almost nothing.

A founder can now paste a 40-page financing agreement into a model and get an attorney-grade read on the covenants. They can run a term sheet and proposed pricing through analysis that would have required a seasoned CFO. The owner who could never justify a full-time CFO — and once reached for the fractional-CFO market — can now co-pilot the business with an agent that never sleeps. Fintechs, ISOs and SMB originators, banks, factors and ABL shops, accountants and consultants: everyone is holding the same tools at the same time.

For a capital partner, that’s not a threat — it’s an invitation. A more informed borrower is a better borrower. The firms that win in this market are the ones who welcome the scrutiny: transparent terms, structures that actually fit, and a willingness to explain the “why” behind every number.

The SaaSapocalypse: when software stops compounding

The agent shift is already showing up in the numbers. For two decades, software-as-a-service grew on the back of switching costs — once your data lived in a vendor’s system, leaving was painful. Agents collapse that moat: when an AI can migrate your CRM, accounting, and project data in a single instruction, the lock-in evaporates. Klarna’s founder put it bluntly — in an agentic world, “SaaS is dead” — and public-market growth is bending to match.

Public SaaS median revenue growth is decelerating

Public SaaS median year-over-year revenue growth, SaaS Capital Index. 2021 and 2022 figures approximate; 2023–2025 per SaaS Capital.

The displacement is real on both sides of the ledger. Salesforce CEO Marc Benioff says AI agents now do 30–50% of the work inside Salesforce and resolve the bulk of its support cases; reporting tied roughly 50,000 U.S. white-collar job cuts in 2025 to AI. Not every bet has paid off cleanly — Klarna walked part of its automation back to a hybrid model after service quality slipped — but the direction is unmistakable. This is not just a reshuffling of IT budgets; it is software beginning to take a share of labor itself.

The market is pricing it accordingly. The AI agents market is projected to grow from $7.84 billion in 2025 to $52.62 billion by 2030 — a 46.3% CAGR, with vertical, industry-specific agents the fastest-growing segment, per MarketsandMarkets.

And the agents are already for sale. OpenAI’s GPT Store hosts roughly 3 million custom GPTs; Salesforce’s AgentExchange launched with 200+ partners and a growing catalog of agents and skills; marketplaces like PromptBase list 270,000+ prompts. Capability is becoming a commodity you can rent by the task.

The tailwinds: policy and power are pushing the same direction

Two forces are pouring fuel on this.

Policy. The One Big Beautiful Bill Act (signed July 2025) restored immediate expensing of domestic R&D (while keeping foreign R&D on a 15-year amortization) — a direct subsidy to building AI in America. It also expanded the Qualified Small Business Stock exclusion to the greater of $15 million or 10× basis, with new partial exclusions at shorter holding periods. Translation: founders and investors who build domestic, growth-stage AI companies keep more of what they create. (IRS overview.)

Power. Intelligence runs on electricity. The IEA projects global data-center electricity use near 945 TWh by 2030; Goldman Sachs sees data-center power demand rising ~165% by 2030 and ~$720B of grid investment; U.S. utilities alone plan ~$1.4 trillion in build-out. That is an enormous, multi-year, capital-hungry expansion — and most of it flows through real businesses: contractors, equipment suppliers, logistics, electrical and mechanical firms, HVAC and cooling, data and security providers.

Capital for the AI build-out

AI adoption is no longer a future planning item — it is a present-day investment decision. Strip away the hype and a practical truth remains: capturing this shift costs money. Development and infrastructure. Talent and compute. Automation, equipment, and inventory. And the working capital required to turn AI capability into revenue — bridging the gap between the investment you make today and the revenue it unlocks tomorrow. This is true whether you’re a manufacturer adding automation, an IT or software firm shipping agentic products, a HealthTech company scaling a platform, a supply-chain operator modernizing logistics, or a consultancy retooling its delivery model.

The businesses that move now will take share. The ones that wait for the old financing playbook to catch up may find the window has closed.

Capital Source: built for the AI era

This is exactly the moment Capital Source was built for. We finance growth-stage and lower-middle-market businesses across every vertical touched by AI — manufacturing, IT and software, HealthTech, supply chain, professional services and consulting — with capital structured around the business, not forced into a rigid product box.

Capital Source is currently accepting applications from AI developers and businesses with defined AI use cases, infrastructure needs, and enterprise investment objectives. Whether you’re building AI-enabled products or modernizing your company around agentic workflows, our Deal Desk can structure capital around your real situation. Apply online →

And we practice what this article preaches. Our Deal Desk pairs seasoned underwriters and structuring specialists with the same secure, intelligent technology reshaping the rest of the economy — reading the full credit story, moving with speed, and designing capital around your cash flow and growth plan. We don’t just fund AI-era businesses; we operate like one. The goal is simple: give founders and operators both the capital and the partnership to compete in a market that’s moving faster than ever.

Capital Source finances AI development.

In AI time, the market moves quickly — the businesses that plan their capital strategy now will be better positioned to build, adapt, and compete. Whether you’re scaling an AI-driven business or financing the build-out around it, our Deal Desk will structure capital around your real situation.

The whole shift, on one page

Click to view full size. This infographic was generated with AI from our article and is provided for general information only — it is not financial advice; availability, amounts, structures, and terms depend on each business’s circumstances and are subject to review and approval.

Takeaways

- The interface is dying. Software is becoming capabilities that agents operate — MCP is the standard wiring it together.

- The playing field leveled. Every owner and advisor now wields frontier-grade AI; transparency and fit win.

- Value is shifting from seats to outcomes. SaaS growth is decelerating as agents take work — and a slice of labor — not just budget.

- Policy and power favor builders. Domestic R&D expensing, expanded QSBS, and a trillion-dollar infrastructure cycle reward businesses that move now.

- It all takes capital. The edge goes to operators who can fund the shift — with a partner who understands it.

Sources

- MarketsandMarkets, AI Agents Market worth $52.62 billion by 2030.

- Salesforce, Introducing Salesforce Headless 360; diginomica, Parker Harris on logging into Salesforce.

- Anthropic, Introducing the Model Context Protocol.

- SaaS Capital, The SaaS Capital Index; Inc., Klarna and SaaS; Fortune, Benioff on AI agents.

- Goodwin, OBBBA tax highlights (R&D, QSBS); IRS, OBBB provisions.

- IEA, Energy and AI; Goldman Sachs, AI data-center power demand.

This article is for informational purposes only and does not constitute financial, tax, legal, or investment advice. It contains forward-looking statements and third-party market projections that are inherently uncertain; figures are attributed to their sources as of publication and may change. Capital Source provides commercial financing solutions; availability, amounts, structures, and terms depend on each business’s circumstances and are subject to review and approval.

Leave a Reply